Key points:

- The 2022 Election commitments report shows the individual and combined budget impacts of the election commitments announced by each of the 3 major parties: the Coalition, the Australian Labor Party (Labor), and the Australian Greens (the Greens).

- The report looks at election commitments with a material impact on the Australian Government budget. It shows how the platforms of the parties, if fully implemented, would change the budget position, relative to the starting point just before the election – as presented in the 2022 Pre-election Economic and Fiscal Outlook (PEFO).

- The PBO has identified 41 material election commitments made by the Coalition, 154 made by Labor and 99 made by the Greens.2 As is often the case for the party in government, the Coalition also announced policies in its budget update, released prior to the election, resulting in fewer Coalition commitments included in this report compared to the other major parties.

- The Coalition’s platform, if fully implemented, would be expected to result in slightly smaller deficits over both the 2022–23 Budget forward estimates and medium-term periods compared to the PEFO. This impact, which results from a slight decrease in payments, is negligible as a share of GDP over both periods. The Coalition’s election commitments do not materially change receipts from PEFO levels.

- Labor’s platform, if fully implemented, would result in increased deficits over the same periods relative to the PEFO (a decrease in the underlying cash balance of up to 0.1% of GDP in any year). This change is driven by slightly higher levels of both receipts and payments as a share of GDP.

- The Greens’ platform, if fully implemented, would be expected to result in larger deficits in total over the same period, relative to the PEFO, reflecting higher levels of both receipts and payments as a share of GDP. The impact of the Greens’ commitments on both receipts and payments are significantly higher than the other major parties.

- The commitments made by the independent member for Indi, Dr Helen Haines MP, form the inaugural ‘Minor parties and independents’ section of the report.

The 2022 Election commitments report shows the individual and combined budget impacts of the election commitments announced by each of the 3 major political parties (the Coalition, the Australian Labor Party and the Australian Greens).

The report adds to the information published by parties about the financial impacts of their election commitments, taking a longer term perspective and presenting a richer view of the impacts on the budget for all major parties on a comparable basis. Box 1 explains the wider fiscal perspectives, and some key concepts used in the report.

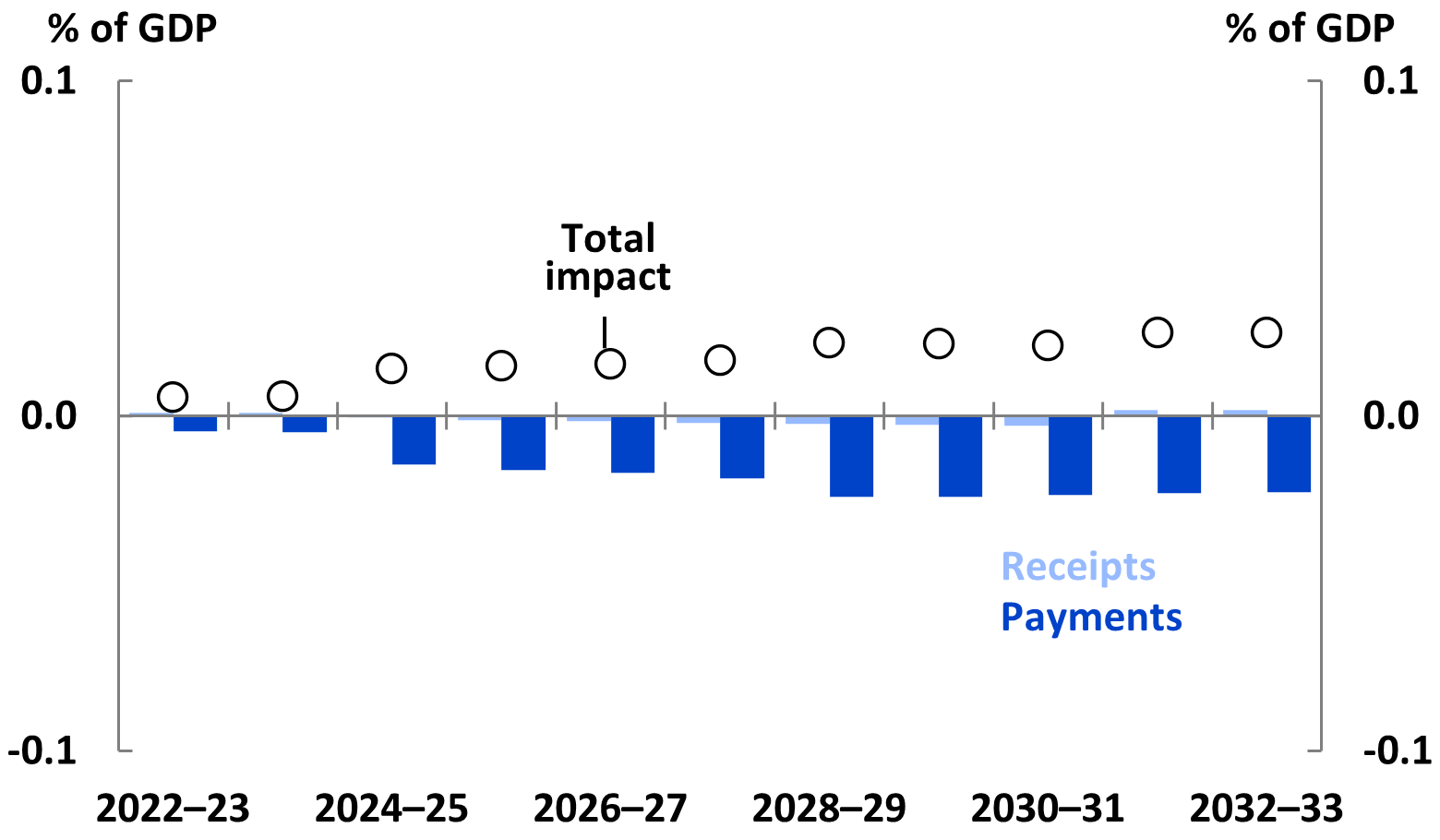

The Coalition’s platform, if fully delivered, would be expected to slightly increase the underlying cash balance (that is, slightly reduce the underlying cash balance deficits) over the 2022–23 Budget forward estimates and medium-term periods, compared to PEFO. The impact is negligible as a share of GDP over both periods. Some of the Coalition’s announcements during the election campaign did not involve any additional fiscal impact as they had already been included in the budget baseline at PEFO.

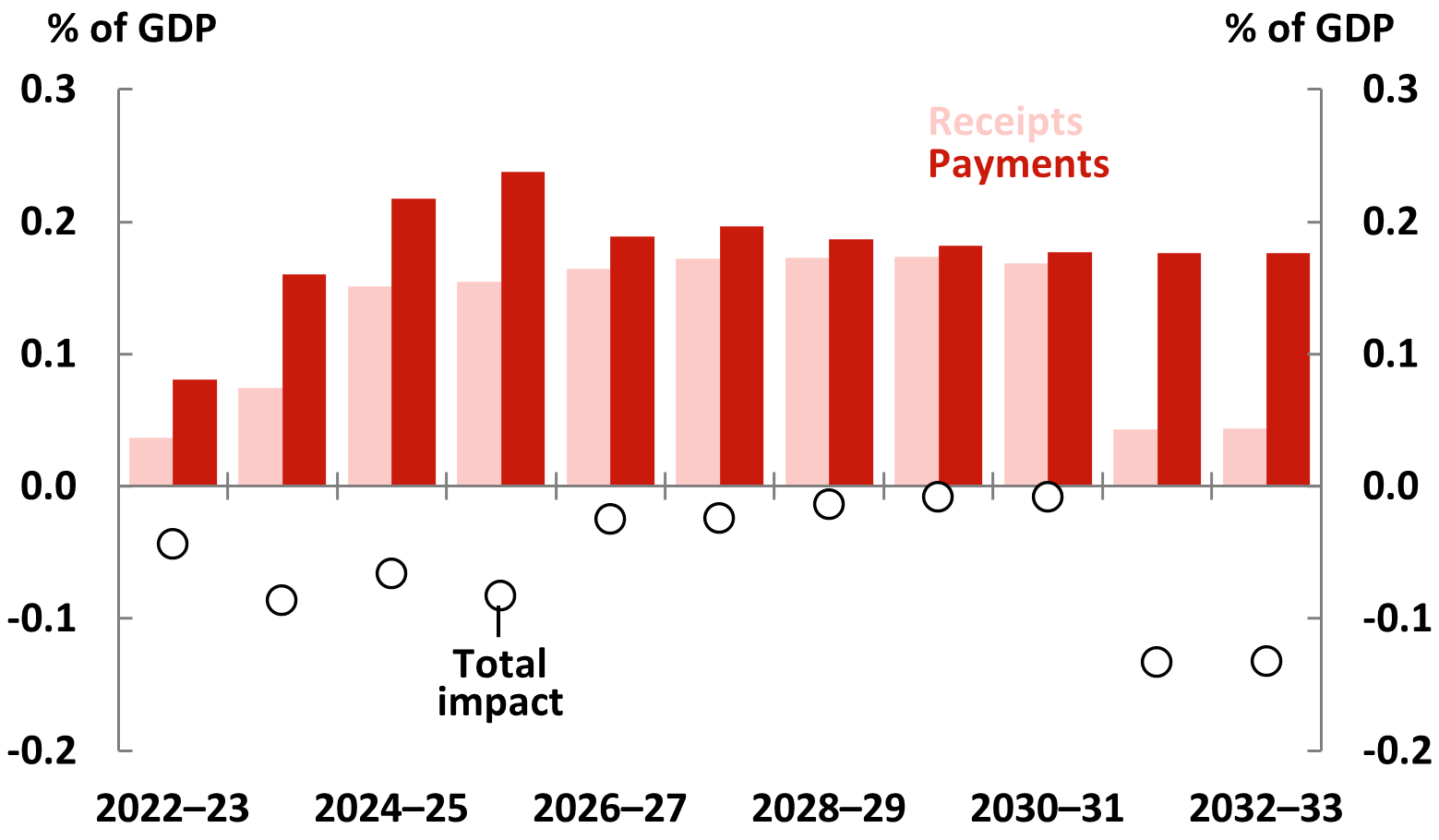

Labor’s platform, if fully delivered, would result in an expected decrease in the underlying cash balance (that is, a larger deficit) relative to the pre-election starting point. This decrease represents up to 0.1% of GDP in any year over the forward estimates and medium-term periods.

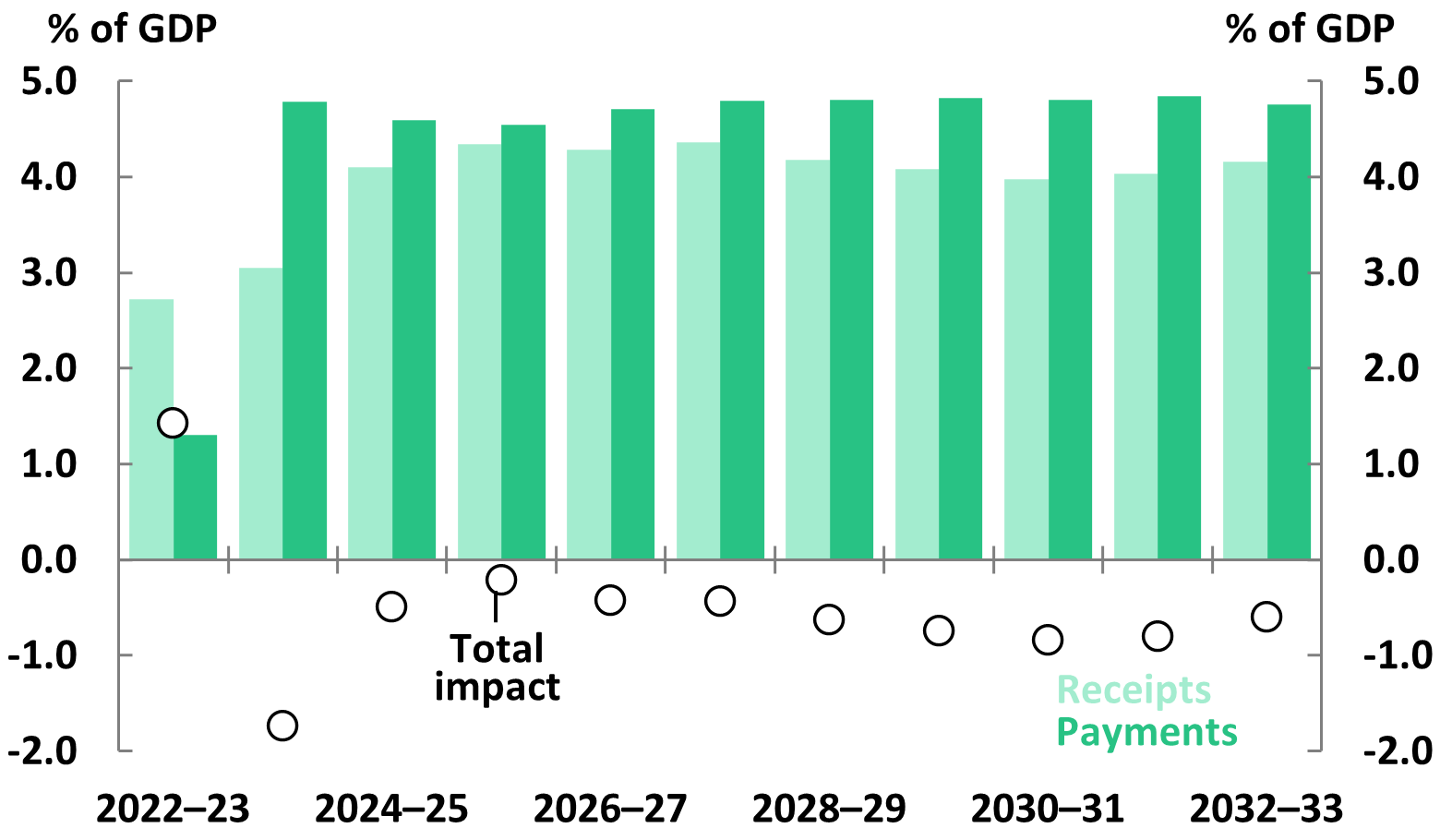

The Greens’ platform, if fully delivered, would be expected to decrease the underlying cash balance over both the 2022–23 Budget forward estimates and medium-term periods compared to PEFO, with an average decrease of 0.5% of GDP per year over the medium term.

The rest of this section provides additional high-level information about the budget impact of party platforms over the forward estimates and medium term. This information is expanded in each party section and the requirements and the methods for preparing the report are at Appendix I. Related terms are explained in the Glossary in this report, which draws from the PBO’s online budget glossary.

Box 1: The Election commitments report: key features and interpretation

This report complements the information about the financial impacts of election commitments published by parties during the election campaign by providing a wider range of information over a longer time period.

The report presents budget impacts over the 2022–23 Budget forward estimates period (the budget year plus the next 3years) and the medium term (the budget year plus the next 10years).

Across both time horizons, we present results for 3 different budget balances – the underlying cash balance, headline cash balance and fiscal balance – to provide a more complete picture of the financial impacts.

When people talk about the budget surplus or deficit, they are often talking about the underlying cash balance. Each of the 3 balances presented here focuses on a different type of financial information, but no one of them provides all the potentially relevant financial impacts. In particular, the headline cash balance is the only balance to show the upfront impact of government loans and equity injections.

The report describes the impacts of individual commitments, and parties’ platforms as a whole, on the budget surplus or deficit. Throughout the report, an ‘increase’ in the budget balance makes the deficit smaller, and a ‘decrease’ in the budget balance makes the deficit larger.

The financial impacts presented here are ‘point in time’ estimates of the commitments based on the commitments as announced during the election campaign. Where these policies are subsequently implemented, their financial implications may change for reasons including updated budget parameters, and the finalisation of policies during further consultation and detailed design stages.

Impacts of election commitments over the forward estimates

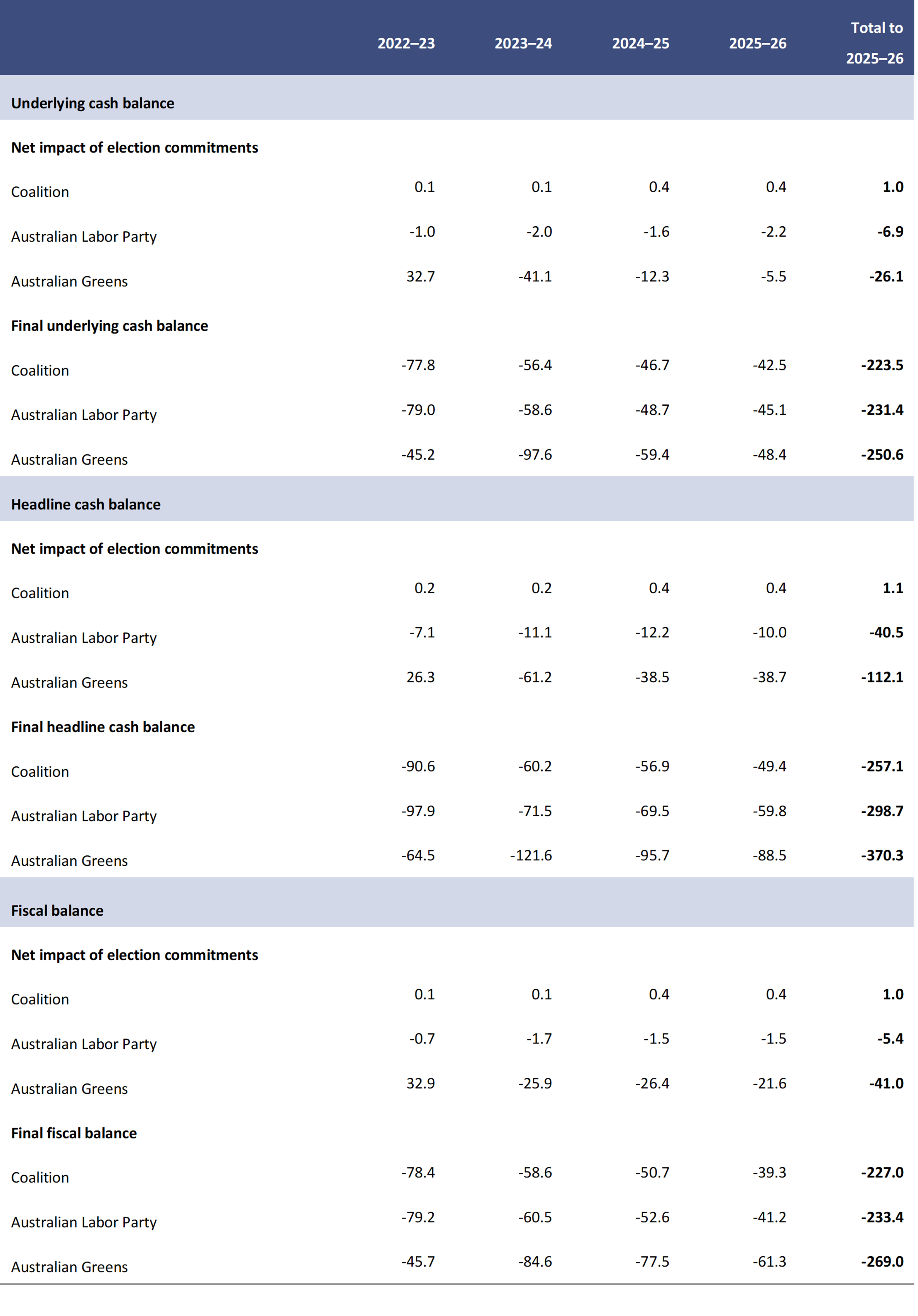

The PBO’s estimates of the total combined budget impact of the election commitments of each party and the resulting level of the underlying cash balance, headline cash balance and fiscal balance over the forward estimates period are shown in Table 1.3,4 A positive impact on the underlying cash balance indicates a larger surplus (or smaller deficit). A negative impact indicates smaller surplus (or larger deficit).

Table 1: Financial implications of election commitments by party, 2022–23 forward estimates underlying cash, headline cash and fiscal balance basis ($billion)

Note: A positive impact indicates an increase in the budget balance. A negative impact indicates a reduction in the budget balance. Figures may not sum to totals due to rounding.

Impacts of election commitments over the medium term

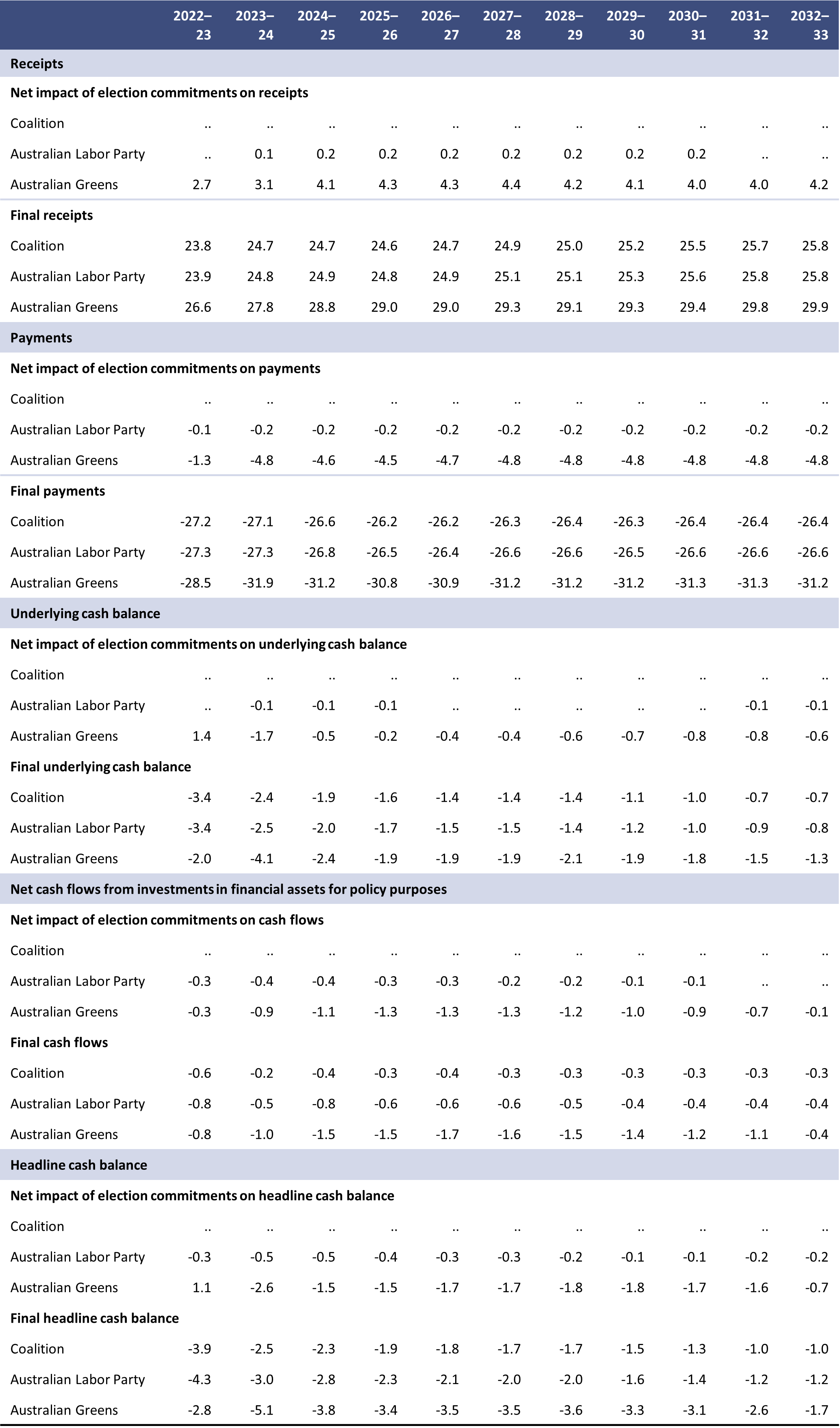

Table 2 shows the PBO’s estimates of the budget impact of each party’s election platform over the medium term (that is, to 2032–33) and the resulting level of the underlying cash balance and headline cash balance as a share of GDP. This table also shows impacts on payments and receipts. The fiscal balance equivalents are shown in Table 3.

Publishing medium-term projections of the fiscal impact of commitments is the PBO’s standard practice for all costings provided outside of the caretaker period, consistent with the PBO’s role of increasing transparency around the budget and fiscal matters.5 Box 2 provides further information on the role of medium‑term budget impacts, including the impact of relaxing our assumption that policies without a specified end date would be ongoing.

Table 2: Financial implications of election commitments on the budget balance, receipts and payments by party, medium-term, cash balance basis (% of GDP)

Note: A positive impact indicates an increase in the cash balance. A negative impact indicates a reduction in the cash balance. Figures may not sum to totals due to rounding.

.. Not zero but rounded to zero.

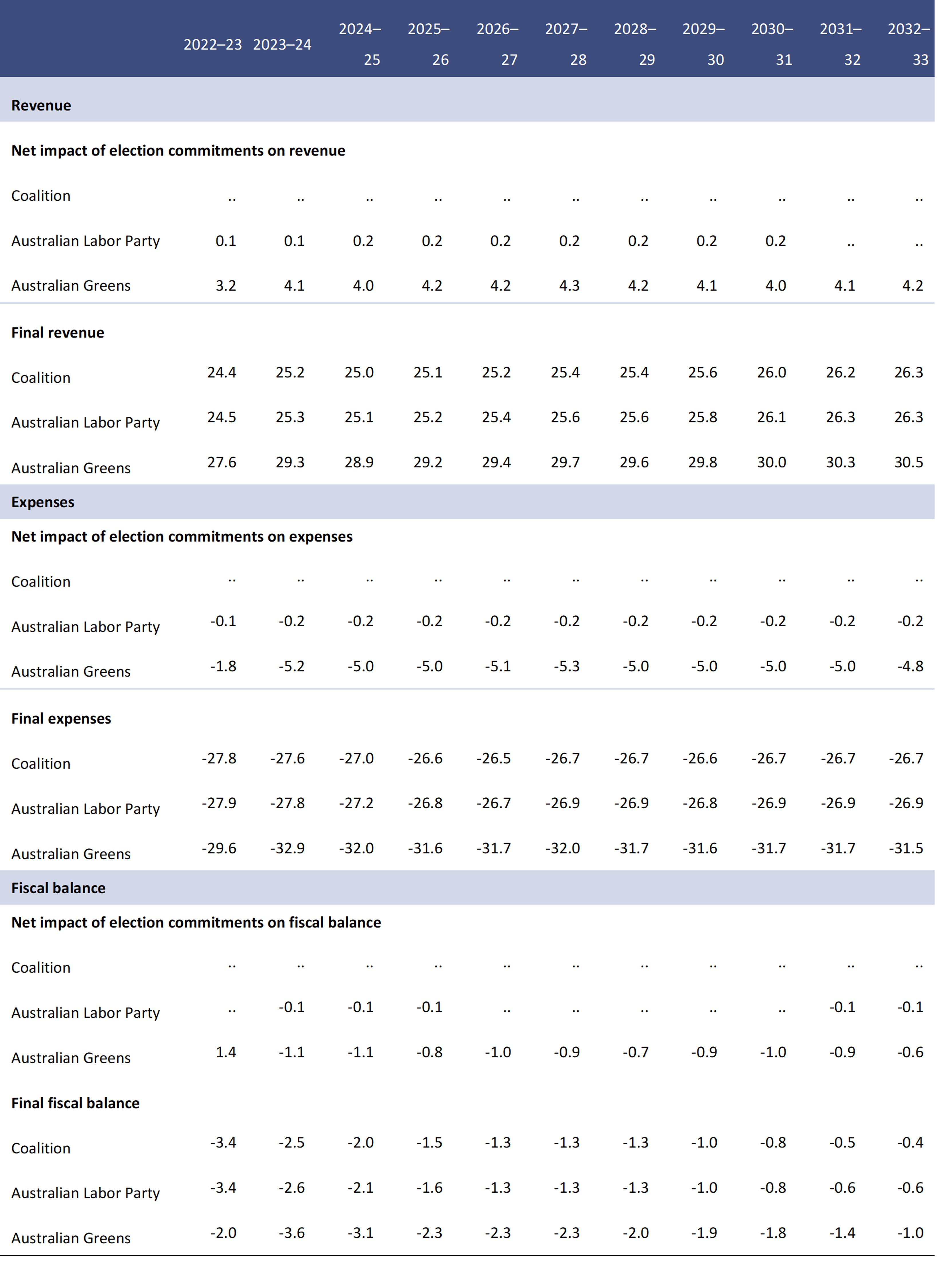

Table 3: Financial implications of election commitments on the budget balance, revenue and expenses by party, medium-term, fiscal balance basis (% of GDP)

Note: A positive impact indicates an increase in the fiscal balance. A negative impact indicates a reduction in the fiscal balance. Figures may not sum to totals due to rounding.

.. Not zero but rounded to zero.

Box 2: The budget impact of commitments over the medium term

The Election commitments report presents the financial impacts of election commitments over the medium term, rather than just the forward estimates. This gives an indication of the trajectory of fiscal policy over the coming decade and can be useful where parties make commitments that may not take effect, or fully mature, until the period beyond the forward estimates. Even when there is a financial impact, it may not always be possible to quantify that impact. In that case, we clearly indicate why we consider the commitment to be unquantifiable.

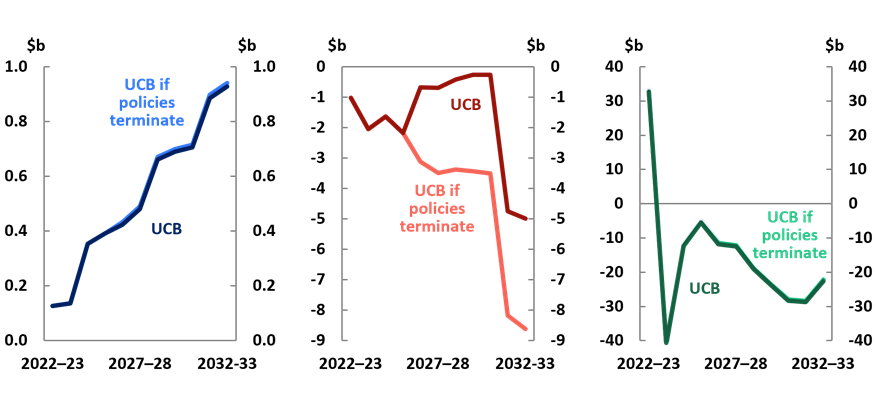

Parties usually make their election announcements transparent, including by publishing detailed material on the purpose and cost of their policies. Nevertheless, the PBO will sometimes need to make assumptions. For example, higher levels of transparency are achieved when parties are specific about the duration of their policies. In some cases, it is not clear from announcements whether a policy would be ongoing or would cease (for example, at the end of the forward estimates). In these cases, when estimating the impacts for the report, the PBO applies our published guidance, by assuming that the policy would be ongoing.6 This assumption has been applied to 48 quantified commitments: 1 for the Coalition, 41 for Labor, and 6 for the Greens.7

Over the medium term, the impact of the PBO’s assumption on each party’s platform on the underlying cash balance results in additional net savings of $21.7 billion for Labor, additional net costs of $74 million for the Coalition, and additional net costs of $2.5 billion for the Greens (Figure 1).

Figure 1: Net impact of PBO guidance on the underlying cash balance (UCB), by party

Coalition Australian Labor Party Australian Greens

Note: See Appendix I for further information about the method for this sensitivity analysis.

For Labor, this resulting improved position was mostly driven by assuming the extension of the major savings commitments Extend and boost existing ATO programs (ECR161) and Savings from External Labour (ECR170), partly offset by additional costs from Powering Australia – Electric Car Discount (ECR124) and other commitments. For the Coalition, the result is driven entirely by Mental Health – Additional Funding (ECR100). For the Greens, the additional cost is driven mainly by LGBTIQA+ Equality (ECR562).

Figure 2 illustrates Tables 2 and 3, showing the impact of election commitments on receipts, payments and the underlying cash balance for each party by year over the medium term.

Figure 2: Medium-term impact of election commitments, by party

Underlying cash balance, 2022–23 to 2032–33

Coalition

Australian Labor Party

Australian Greens

Impact of party platforms on receipts, including interactions with the tax cap

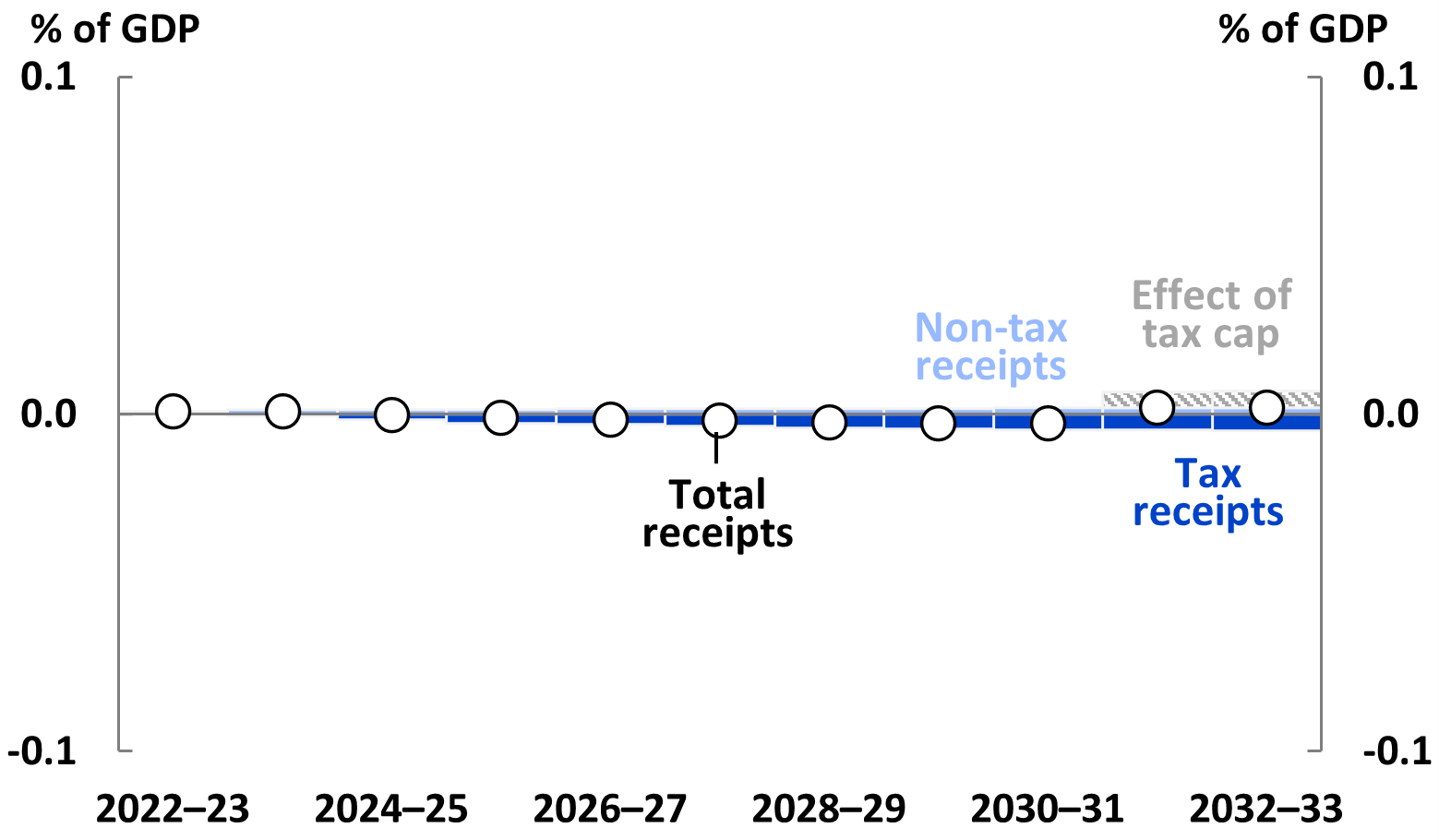

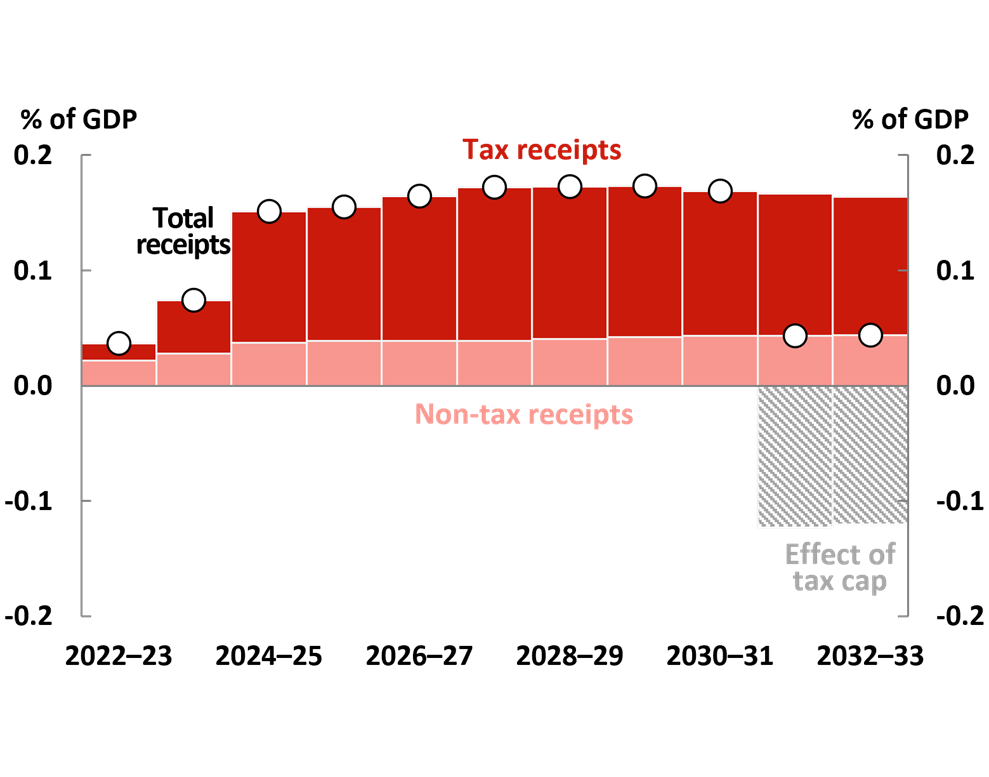

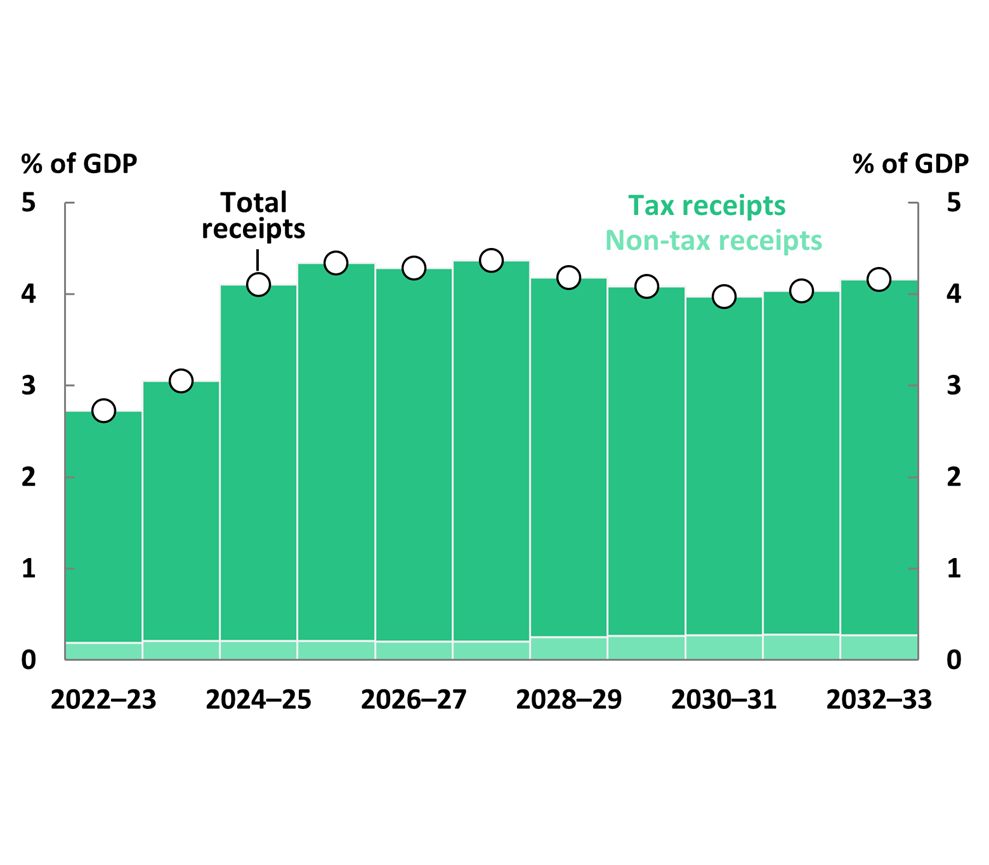

Figure 3 shows the impact of each major party’s policies on receipts in each year and whether these are tax or non-tax receipts.

These impacts take into account each party’s commitments about the tax-to-GDP ratio. See Box 3 for further explanation and a stylised example of how the application of the tax cap affects the budget balance.

Box 3: Tax caps and the budget balance

In the absence of policy change, tax receipts tend to increase over time, mainly due to the impact of bracket creep.8 As part of their medium-term fiscal strategies, successive governments have committed to maintaining tax receipts as a share of GDP at or below a stated ‘cap’. The budget projections therefore implicitly incorporate ‘unspecified tax cuts’ once the cap is reached.

The former Government committed to maintain tax receipts at or below a cap of 23.9% of GDP, so this cap forms part of the PEFO baseline. Labor has no policy to change the tax cap while the Greens do not support a tax cap.9,10

In the 2022 PEFO, tax receipts were projected to reach the 23.9% tax-to-GDP cap in 2031–32 and stay at that level for the remaining year of PEFO projections. As a result, if parties have different policies around a tax cap relative to the Coalition, it will affect the total budget impact of that party’s election platform from 2031–32.

To see how this works using a stylised example, suppose there are 2 parties who make the same election commitments with just one difference — one party is committed to a tax cap and the other is not. Once tax receipts reach the cap it would only apply for the party supporting the cap, with the result that they would have lower projected tax receipts, and therefore overall receipts, than the party without the tax cap. Since the budget balance is the difference between payments and receipts, the party with the tax cap would have a lower budget surplus (or higher deficit) than the party that did not support the cap.

Labor’s receipts commitments are expected to result mostly in a small increase in tax receipts. Commitments including Extend and boost existing ATO programs (ECR161) and Plan to ensure Multinationals Pay Their Fair Share of Tax (ECR167) result in tax receipts increasing by around 0.1% of GDP in most years compared to the budget baseline, before returning to baseline levels in 2031–32 as tax receipts reach the 23.9% tax-to-GDP cap (the same year as the Coalition).

In contrast, the Greens anticipate raising significantly more tax receipts, equivalent to around 3.7% of GDP in most years. The Greens included major tax changes in their election platform, including commitments to reverse the stage 3 tax cuts in their commitment A Fair and Progressive Income Tax System (ECR539), introduce a super profits tax in “Tycoon” Super Profits Tax (ECR534) and Mining Super Profits Tax (ECR535), as well as introduce a wealth tax on billionaires in Billionaires Tax (ECR533).

Figure 3: Impact of party platform on receipts, by major receipt type

Underlying cash balance, 2022–23 to 2032–33

Coalition

Australian Labor Party

Australian Greens

Note: Tax receipts include income derived from taxes; such as company tax, personal income tax, and goods and services tax. Income from other sources is included in non‑tax receipts; such as royalties, interest earned on loans and dividends from investments. See ‘Aggregating election commitments’ in Appendix I for information on the application of the tax cap.

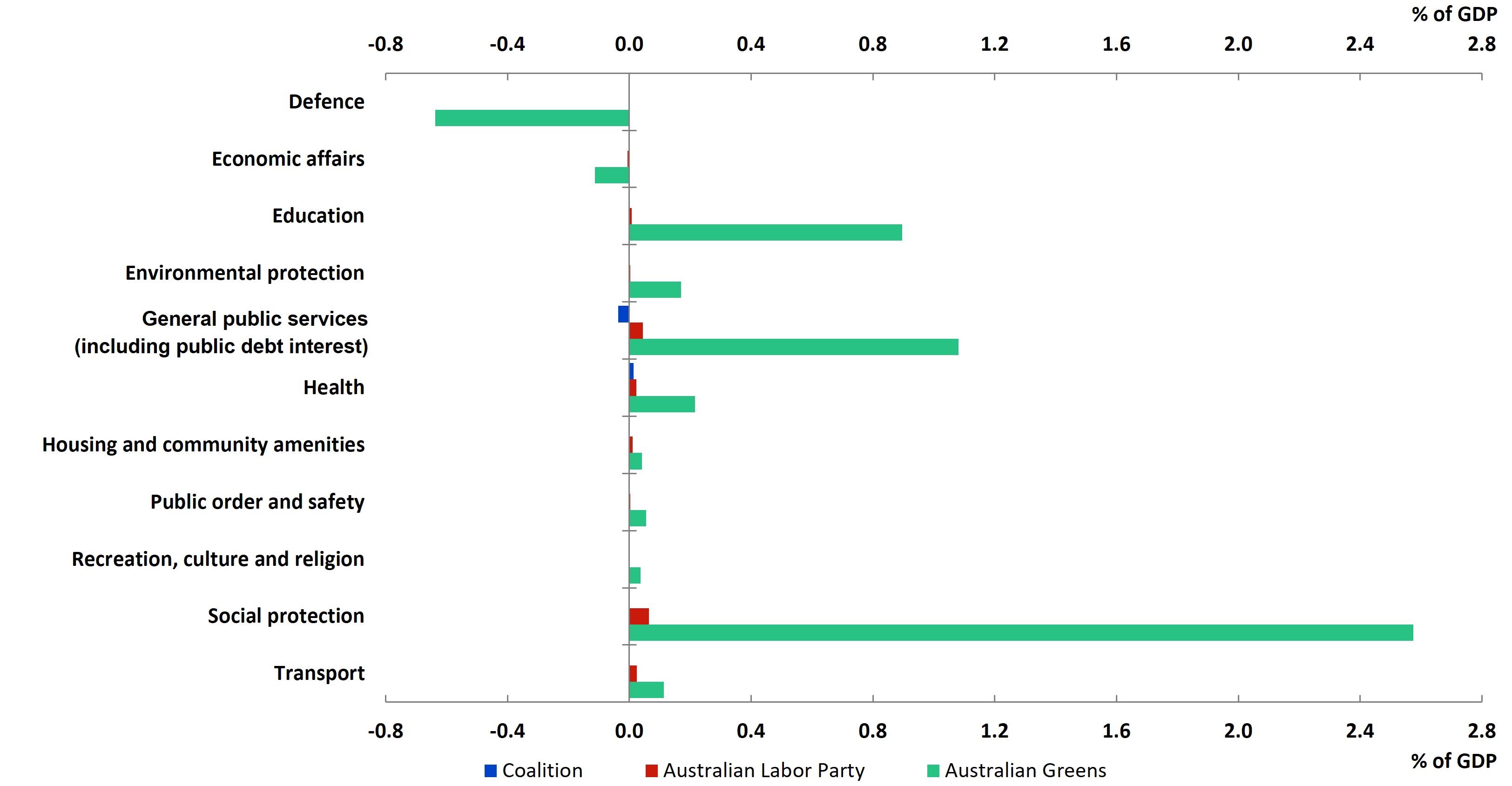

Impact of party platforms on payments

Figure 4 shows the impact on payments of each major party’s policies according to their primary purpose, using the standard Australian Bureau of Statistics classification for government spending.11

The Coalition’s largest payments commitment, Agency Resourcing (ECR002), reduces funding under general public services through the efficiency dividend. Overall, Coalition commitments have a negligible net impact on total payments as a share of GDP, with part of these savings from general public services offset by the health commitments Reducing the PBS Co-Payment (ECR004) and Expansion of the Continuous Glucose Monitoring Initiative (ECR003).

Labor’s additional spending is mostly in social protection, general public services and health. This increase reflects spending on social programs through Cheaper Child Care (ECR115) and Fixing the Aged Care Crisis (ECR146), and additional departmental funding for the Australian Taxation Office to carry out taxation compliance activities under Extend and boost existing ATO programs (ECR161).

The Greens committed to significantly higher spending overall, partly funded through higher receipts and a reprioritisation of funding from defence and economic affairs. In the defence category, the commitment Peace, Disarmament and Demilitarisation (ECR565) reduces defence funding to 1.5% of GDP. The reprioritisation from the economic affairs category mainly reflects the abolition of fuel tax credits in End handouts for coal, oil and gas companies (ECR502). Increases in payments are mainly directed to social protection, general public services and education. For social protection, the additional spending is equivalent to 2.5% of GDP in an average year, and mostly comprises increases to social welfare payment rates in No One in Poverty (ECR558). Increases in the general public services and education categories are equivalent to around 1% of GDP a year. The largest contribution to the increase in spending on general public services comes from increasing Australia’s foreign aid funding in Human Rights and Increase Foreign Aid (ECR564), while the largest contribution to education spending is for Free TAFE and University (ECR528).

Figure 4: Impact of party platform on payments according to purpose

Underlying cash balance, average annual impact 2022–23 to 2032–33

Note: Spending is allocated according to the Classification of the Functions of Government – Australia, consistent with the framework underpinning the Australian Bureau of Statistics’ Government Finance Statistics. Where commitments cover multiple purposes, they have been allocated to the primary category according to the relative dollar value.

Final levels of spending for 2020–21 were: Defence $40.7bn; Economic affairs $100.6bn; Education $47.9bn; Environmental protection $6.9bn; General public services $115.7bn; Health $97.0bn; Housing and community amenities $2.8bn; Public order and safety $6.9bn; Recreation, culture and religion $4.1bn; Social protection $226.1bn; and Transport $12.1bn.

Material divergences from estimates made public prior to polling day

For the Coalition and Labor, the level of the underlying cash balance over the forward estimates period presented here is not materially different from the estimates released by the parties prior to polling day.12

While the Greens did not publish a consolidated fiscal plan prior to polling day, their announcements included estimated budget impacts and these are in line with the impacts in this report.13 Differences in the estimates predominantly arose because the Greens’ announced estimates were costed before the release of the 2022–23 Budget and therefore used slightly different economic parameters and a different forward estimates period.

No party released consolidated estimates of the medium‑term impacts of their election commitments prior to polling day.

Further information on announced election platforms

This section provides an overview of features such as the use of balance sheet financing to fund election commitments, the inclusion of distributional analysis in the report, methodological issues such as the identification of election commitments, assessing the materiality of commitments, and the approach to capped funding commitments. Appendix I provides further detail on the PBO’s method and approach.

Commitments funded through balance sheet financing arrangements

There has been an increase in the use of balance sheet financing arrangements, such as loans, equity injections and guarantees, to fund policy priorities over the past decade and all major parties announced commitments involving the use of balance sheet financing arrangements during this election period.

The budget impacts of these commitments can be understated when looking at the fiscal or underlying cash balance impacts alone.14 The headline cash balance impact, presented above and in the appendices for each party, provides a better indication of the cost of the initial contribution. Greater use of balance sheet financing arrangements will usually result in headline cash balance impacts that are lower (indicating a worsening budget position) than the underlying cash balance impacts.

For the 2022 election, the Coalition announced 2 commitments involving the use of balance sheet financing arrangements. One of those commitments, Future Farmer Guarantee Scheme (ECR001), replaces part of an existing balance sheet financing arrangement (concessional loans) with another type (guarantees). Because the guarantees decrease the headline cash balance by less than the loans, the overall impact of the Coalition’s 2 balance sheet financing commitments is actually to increase the headline cash balance, and it is $0.1 billion higher than the underlying cash balance impact over the period. Both balance sheet financing policies terminate within the forward estimates and the difference between the headline cash and underlying cash balances is not material over the medium term.

Labor announced 11 quantifiable commitments involving the use of balance sheet financing arrangements. They would result in the headline cash balance being $33.6 billion lower than the underlying cash balance over the forward estimates period, and $62.7 billion lower over the medium term.

The Greens announced 17 such commitments; these result in the headline cash balance being $86.0 billion lower than the underlying cash balance impact over the forward estimates period, and $289.8 billion lower over the medium term.

Distributional impacts of selected commitments

Parties that have previously requested distributional impacts analysis as part of a PBO costing outside of the caretaker period could elect to retain some or all of that information as part of the costing documentation produced as part of this report.

The Greens elected to retain distribution information for 3 commitments: Wipe Student Debt (ECR529), A Fair and Progressive Income Tax System (ECR539), and Hospital Funding and Waiting List Blitz (ECR550). Labor did not elect to retain any distributional information.

Identifying election commitments

The Parliamentary Budget Officer decides which commitments should be included in the election commitment report, based on announcements made by the parties up to polling day and any associated fiscal impact. Election commitments included in the report must be public, specific, and material.

Where no firm commitment is made as to the policy mechanism or details that would deliver on the announcement, it may be considered aspirational in nature. Where an announcement involves detailed actions to achieve an aspirational target, the PBO would include the commitment in the report.

Commitments without a material budget impact

Not all election commitments made by parties have a direct fiscal impact. As the purpose of this report is to identify commitments that are expected to have a significant impact on the fiscal position, commitments that are not material have not been included in this report. There are 4 main reasons that an announcement meeting the other criteria for being a commitment might not be a material commitment for the purposes of the report.

- Commitments introduce regulatory changes (where they can be administered using the current regulatory arrangements).15 The Green’s commitments to ban political donations from certain industries and introduce truth in political advertising laws are examples of regulatory changes.

- The commitment involves only an increase in departmental expenses and this increase could reasonably be expected to be absorbed, or is already provided for, in existing agency budgets. For example, Labor’s commitment to conduct a Waste and Rorts Audit and the Coalition’s commitment to work with stakeholders on the design of amending the criteria for the Home Equity Access Scheme, could be met within existing departmental resources.16

- The commitment is in the PEFO baseline because the announcement is a ‘decision of government’. That is, the decision to implement the proposal was appropriately authorised by the Government prior to the start of the caretaker period.

- The commitment would have no material impact because it reallocates funds which are in the PEFO baseline, but not yet committed to a particular project. Both Labor and the Coalition announced commitments which were already included in the budget baseline, such as the Coalition’s Townsville Hydrogen Hub and Labor’s matching commitment. These were announced during the caretaker period but use existing uncommitted funding under the Energy Security and Regional Development Plan.

Commitments with capped funding or savings

Across all major parties, a considerable number of election commitments involved the commitment of specified (or capped) amounts of funding to achieve particular policy outcomes. These capped amounts, as specified by parties, have been included in the estimates of the budget impact. The PBO has not, however, assessed whether the specified amounts would be sufficient to achieve the announced policy outcomes.

The PBO adopts a similar approach with respect to capped savings proposals, where a specified amount of money is deemed to be saved from reducing the amount of an activity. That is, the PBO confirms that existing expenditure is equal to or greater than the specified saving but does not assess the impacts of reducing expenditure.

Additional detail by party

Detail on the budget impacts of each party’s election platform is set out in the next section, and in the summary tables at Appendices A (Coalition), B (Labor), C (Greens), and D (Independent member for Indi).

Individual costing documents are at Appendices E (Coalition), F (Labor), G (Greens), and H (Independent member for Indi) for all election commitments other than those involving specified (capped) amounts of funding. These costing documents provide the detailed specification, assumptions and methodologies applied in estimating the fiscal impacts of each commitment. The companion Guide to reading PBO costings provides a short overview of PBO costing documents with commentary and examples.

Footnotes

- ‘Designated’ or major parties for the purposes of this report are defined by the Parliamentary Service Act 1999 as those with 5 or more members of Parliament immediately before the election is called. The major parties of the 46th Parliament of Australia were the Coalition, the Australian Labor Party, and the Australian Greens. The Liberal Party of Australia, National Party of Australia, Liberal National Party of Queensland and Country Liberal Party are treated as a single party, the Coalition, for the purpose of this report, in line with the PBO’s legislation.

- Because commitments are primarily those identified by parties, this number is affected by the way that parties choose to group their commitments. For example, making fewer more highly aggregated commitments with many subcomponents would result in a lower number of commitments

- All final budget aggregates for each party exclude unquantifiable commitments, consistent with the budget treatment of unquantifiable measures

- The ‘starting point’ PEFO levels for all balances are included in the more detailed financial tables in

Appendices A to D. - Medium-term estimates were included for a subset of costings in the 2019 election commitments report. The 2019 report also included the total net impact over the medium term of all election commitments for each party, as a share of GDP.

- See the PBO’s general election guidance note 2 of 4, The election commitments report: overview, page 3.

- The PBO’s assumption that a policy is ongoing applies in just one case during the forward estimates period — for the Greens’ Future of Work Commission (ECR600). Table 1 in each of Appendices A to D shows whether a commitment has been assumed ongoing, and from which year.

- See PBO Budget explainer No.1, Bracket creep and its fiscal impact, 29 September 2021.

- The financial impact of each party’s policy on the tax cap is separately identified in Table 2 of Appendices A to D:

Detailed tables showing budget impacts of election commitments. - For more information about the tax cap, see the PBO’s Guide to the Election commitments report. For more

information on the methodology in applying the tax cap see Appendix I – Report requirements and method. - The Classification of the functions of Government – Australia, as per the Australian Bureau of Statistics’ Government Finance Statistics.

- See the Coalition’s budget document Our plan for Responsible Economic Management and Labor’s budget document Plan for a better future.

- These announcements are available in the Greens’ platform.

- Balance sheet financing arrangements can be an appropriate method for financing government commitments, however, the budget reporting of these arrangements is not as comprehensive as the budget reporting of direct expenditure and taxation measures. See PBO report no 01/2020 Alternative financing of government policies - Understanding the fiscal costs and risks of loans, equity injections and guarantees.

- Regulatory changes would be expected to have impacts across the economy, often having offsetting impacts on different sectors. The flow-on effects of these impacts on the budget are referred to as ‘indirect effects’ or ‘broader economic effects’, however the net budget impact of these effects is often highly uncertain in terms of magnitude and timing. For further discussion of these issues, see Appendix I

- While Labor’s Waste and Rorts Audit may result in cost savings, these have not been identified in Labor’s fiscal plan and are not included in this report.